Cybersecurity now occupies executive meetings, extending beyond technical departments. Stories emerge weekly about companies facing ransomware incidents, lost data, deceptive emails, and halted operations due to malicious actors. Even as firms spend on protective tools and training efforts, insight grows – relying only on defense strategies falls short.

Protection is never absolute within any security plan. Firms that operate advanced cyber defenses still face risks from highly complex breaches. Because of this, some teams now consider insurance against digital threats when shaping broader approaches to risk. Still, getting cyber insurance differs greatly from obtaining typical business policies. Because insurers demand proof of solid defenses, firms seek expert advice more often these days. With expectations rising, guidance helps companies meet requirements quietly. Therefore, many rely on consultants who clarify steps without delay. Coverage follows only when safeguards reach acceptable levels steadily

Understanding Cybersecurity Insurance

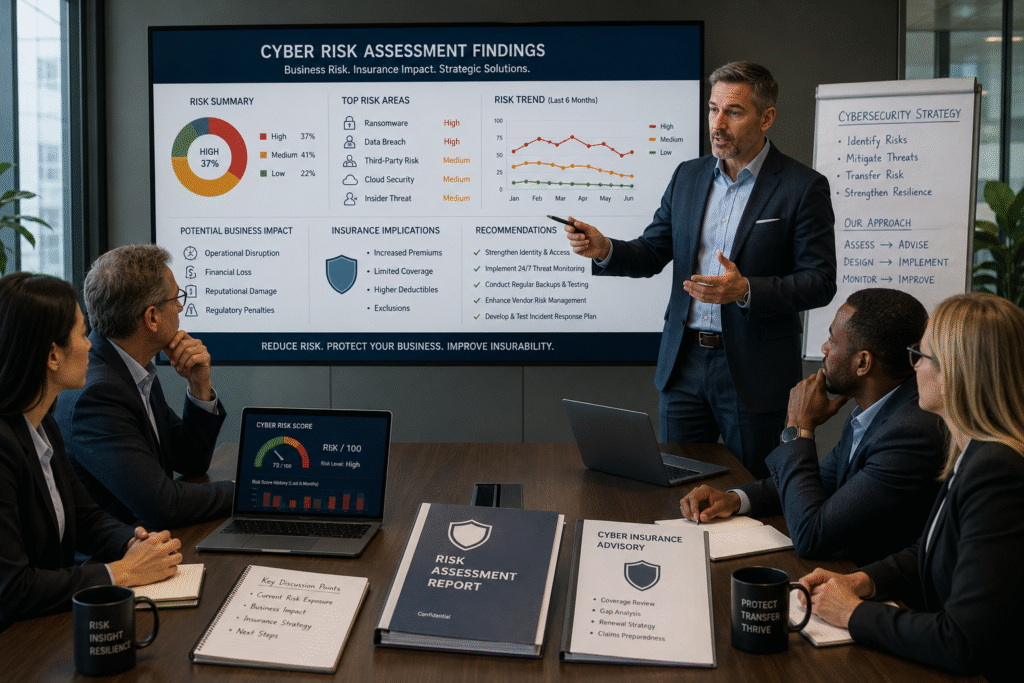

Cybersecurity insurance, sometimes called cyber liability protection, supports companies facing financial strain due to digital threats. Coverage varies by plan but might address expenses tied to leaked information, malware demands, court-related spending, fines imposed by authorities, system analysis during crises, managing public image, along with halted operations. While one provider emphasizes recovery logistics, another focuses on upfront defense funding – each structured differently behind the scenes.

It is common for companies to face serious monetary consequences after a cyber breach. Operations might stop entirely during a ransomware event, lasting several days or longer. Trust among clients often declines when security fails. Authorities could begin reviewing compliance matters afterward. Costs related to fixing systems sometimes grow far beyond early estimates.

Cyber insurance offers protection against certain expenses tied to digital threats. Still, its value emerges only when policies match an organization’s needs closely. Meeting every condition set by the provider shapes how well it functions during incidents.

cyber insurance matters more now

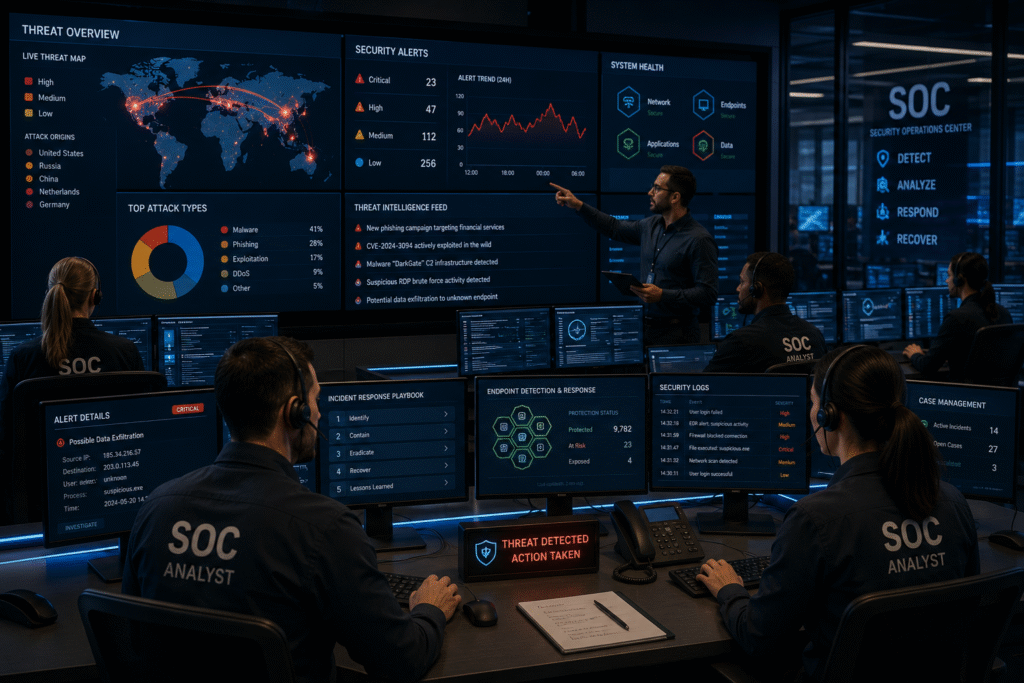

Over ten years, digital dangers have shifted greatly. Not just big firms face risks now. Smaller companies see more attacks due to limited protection tools. Weak safeguards make them easier targets than before.

Meanwhile, rules around safeguarding data keep shifting. Firms managing personal details, monetary records, medical files, or critical proprietary knowledge encounter increasing requirements to comply.

Unexpected delays often follow a breach, affecting daily operations. When systems fail, work slows without warning. Financial setbacks appear through fines or lost revenue. Rebuilding trust takes time after private information is exposed. Customers might reconsider their loyalty. Legal actions sometimes arise from inadequate protection. Long-term reputation damage lingers even after fixes are applied. Recovery includes more than restoring files – it involves relationships

➤ Extended operational downtime

➤ Loss of customer confidence

➤ Legal and regulatory challenges

➤ Revenue disruption

➤ Increased recovery costs

➤ Reputational damage

Long after systems come back online, monetary consequences often continue to unfold. When disruptions strike, cyber insurance supports recovery by adding a buffer against such lingering effects.

The Rising Demands From Insurance Companies

It is often thought securing cyber insurance means completing a form and covering the cost. Yet providers now apply stricter criteria when offering coverage.

With rising numbers of cyber incidents, evaluations by insurers grow stricter. Because threats carry higher expenses, scrutiny increases during applications. When reviewing firms, focus shifts toward active risk control measures. Instead of depending only on policies, companies must show consistent efforts. Since protection gaps appear more often, proof of management practices matters greatly. Where digital dangers spread quickly, passive approaches fail inspections. Though coverage remains an option, evidence of prevention becomes essential.

Today, insurers commonly evaluate areas such as:

➤ Multi-factor authentication implementation

➤ Endpoint protection capabilities

➤ Vulnerability management processes

➤ Security awareness training programs

➤ Backup and disaster recovery procedures

➤ Incident response planning

➤ Access control management

➤ Email security controls

Should these safeguards remain unproven, firms might encounter steeper costs, reduced protection, or outright rejection of insurance terms.

Here, guidance on cyber risk coverage gains clear importance.

Understanding Cybersecurity Insurance Guidance?

A focused guidance on cyber insurance supports companies as they navigate coverage requirements, at the same time strengthening digital defenses. While applying for policies, firms gain insight into risk reduction methods through tailored evaluations. This type of support emerges when financial protection meets security readiness, shaping resilience across operations. Preparation becomes part of strategy, rather than an afterthought during claims. Insights form gradually, aligning policy needs with real-world threats facing modern systems.

Instead of merely choosing a policy, advisors assess operational vulnerabilities alongside structural exposures. To strengthen readiness, they examine how companies manage uncertainty while meeting insurer expectations.

Starting at ground level, one looks first at how security currently functions within a structure. From there, attention shifts toward spotting weak points capable of disrupting workflow. A close examination follows, revealing what threats might interfere. Each step moves carefully through existing safeguards. Insight grows by assessing where exposure exists. Eventually, focus lands on vulnerabilities tied directly to daily function.

Following assessment, advisors measure current safeguards alongside insurer criteria along with recognized standards, pinpointing gaps needing attention prior to submission of applications. Where adjustments are necessary, clarity emerges through structured review rather than assumption.

A clearer path emerges when cyber insurance decisions reflect both risk management needs and strategic priorities. Business goals shape the direction, while security spending follows in measured steps. Insight grows where protection efforts meet organizational aims. Decisions gain clarity through alignment of resources and intent. Outcomes improve once financial safeguards mirror actual operational demands.

What Gets Looked At In An Advisory Review

Not every company faces the same threats, yet typical cybersecurity insurance assessments tend to centre on a handful of key concerns. Despite differences in operations, certain risk factors appear again across evaluations. While priorities may shift slightly, common themes still emerge during consultations. One area often overlaps with another, creating patterns advisors regularly observe. Although each business operates uniquely, repeated elements shape how guidance takes form.

Risk Assessment

A detailed evaluation reveals which resources matter most, along with likely dangers and essential operations. Because of this clarity, decisions about necessary insurance levels become more grounded in actual exposure.

Security Control Evaluation

With careful inspection, current security measures undergo assessment against accepted norms plus insurance criteria. Through this process, gaps may surface – inviting refinement that lowers exposure over time.

Policy and Compliance Check

Compliance with regulations and internal rules tends to require proof from organizations. When reviewing present methods, advisors determine alignment with required standards.

Coverage Analysis

Some cyber insurance plans differ in what they cover. Because of this, guidance from experts allows firms to see where protections may fall short. These reviews clarify restrictions within policies, highlight boundaries on payouts, yet also point out unseen vulnerabilities leading to cost risks.

Incident Response Preparedness

Should a breach occur, insurers now expect proof of preparedness. Reviewing how teams react begins with examining response frameworks. Communication workflows come under scrutiny next. Resilience hinges on tested recovery methods. Readiness shows in structured protocols, not promises.

Benefits Beyond Insurance

Among overlooked elements in cybersecurity insurance guidance stands its benefit outside securing coverage. What often escapes attention is how advice in this field extends past mere policy acquisition. Rarely noted, yet present, lies support that goes further than paperwork. It exists not just in documents but in foresight offered along the way. Beyond the contract emerges insight shaping readiness. Hidden within counsel is preparation not tied to forms. Value surfaces where least expected – before any claim arises.

Occasionally, guidance reveals flaws companies did not see. When corrected, ripple effects improve wider operations.

Benefits commonly include:

Improved Security Posture With better insight into weaknesses, companies find it easier to decide where security spending matters most.

Reduced Risk Exposure

Greater oversight reduces chances of digital breaches while also limiting operational impact. A firm grip on systems lessens risk exposure alongside possible downtime effects. When safeguards improve, threats find fewer openings yet consequences stay contained. Tighter rules tend to block intrusions even as they narrow fallout scope. Security advances often prevent hacks although disruptions shrink too.

Better Regulatory Readiness

Where insurers demand certain cybersecurity measures, those same steps often align with legal requirements. Compliance gains momentum when security practices meet external expectations. Not every rule comes from legislation – some emerge through insurance conditions. When safeguards satisfy underwriters, they frequently address regulatory concerns too. Requirements imposed by policies can quietly reinforce statutory obligations behind the scenes.

Enhanced Business Resilience

When systems fail, faster recovery becomes possible through refined response strategies. Organizations adjust promptly because preparation meets practical execution. Resilience grows where plans are clear yet adaptable. Speed follows structure during unexpected events.

Increased Executive Visibility

Understanding of cybersecurity improves when explained clearly for leaders, which aids choices. Because clarity rises, communication grows more effective among executives. When ideas simplify, decisions rest on stronger awareness. With better framing, technology risks make sense to those guiding strategy. As explanations shift, insight deepens without extra complexity.

Common Challenges Organizations Face

Throughout evaluations for cyber risk coverage, certain difficulties emerge with regularity.

Outdated security policies remain in place at certain institutions, despite shifting threat landscapes. Where asset tracking lacks completeness, identifying critical protections becomes unclear instead.

One issue still stands out: employees often lack proper awareness. Despite sophisticated tools existing, mistakes made by people contribute heavily to cybersecurity problems.

Yet another factor involves the mistaken belief that technology solutions meet all insurance demands. Instead, attention spreads across management practices, workflow consistency, together with preparedness in daily operations. Should signs of difficulty appear sooner rather than later, firms may respond ahead of any effect on coverage access or daily function. Early awareness opens space for adjustment prior to disruption in policy qualification or workflow continuity

Looking Ahead

Should cyber threats keep shifting, insurers may raise their demands accordingly. Firms viewing cybersecurity coverage within wider risk planning stand a stronger chance of adjusting smoothly. What matters most is alignment across policies and preparedness.

Instead of treating cyber insurance merely as a financial tool, companies might consider it a chance to reinforce defenses. Security habits could grow stronger through such coverage. Resilience often follows when protocols are reviewed under its lens. Long-term planning gains depth when risks are reassessed regularly. A different view on protection emerges – not just compensation after harm occurs.

Conclusion

What once seemed a benefit only big companies could access now matters to organizations of every size. Protection through cyber insurance plays a central role in how businesses handle digital threats today. Still, simply filling out forms and sending payments does not guarantee useful protection.

Security demands clear awareness of threats, consistent control practices, yet readiness through structured incident response planning. While risk understanding forms a base, operational safeguards follow, along with prepared reactions when events occur. With every threat comes the need for both vigilance and methodical preparation, because systems face constant pressure. Response capability does not appear without prior design; instead, it emerges from ongoing effort paired with foresight into possible failures.